The business auto insurance coverage line has struggled to realize underwriting profitability for years, even earlier than the inflationary circumstances which have been affecting property/casualty strains extra just lately. This development has been accompanied by regular development in internet written premiums (NWP).

This weak spot in underwriting profitability has been pushed by a number of causes, in keeping with a brand new Triple-I Points Transient. One is the truth that automobiles – each business automobiles and private automobiles they collide with – have develop into more and more costly to restore, because of new supplies and elevated reliance on sensors and laptop methods designed to make driving extra snug and safer. This well-established development has been exacerbated by supply-chain disruptions throughout COVID-19 and persevering with inflation within the pandemic’s aftermath.

Distracted driving and litigation tendencies even have performed a job.

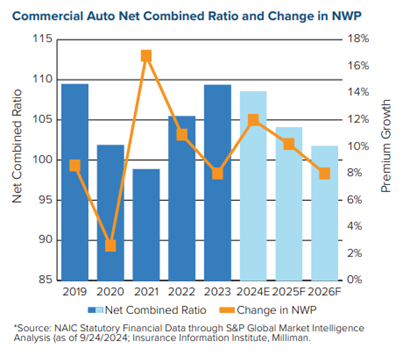

Nevertheless, Triple-I sees some gentle on the horizon for business auto when it comes to the road’s internet mixed ratio – an ordinary measure of underwriting profitability calculated by dividing the sum of claim-related losses and bills by earned premium. A ratio below 100 signifies a revenue and one above 100 signifies a loss.

Because the chart under reveals, the estimated 2024 internet mixed ratio for business auto insurance coverage has improved barely since 2023, and additional enchancment is predicted over the subsequent two years.

These projected enhancements are primarily based on an expectation of continued premium development – due extra to aggressive premium charge enhance than to elevated publicity – as the speed of insured losses ranges off.

{kind=link}