Soar to winners | Soar to methodology

Digital defenders

Cybercriminals work across the clock, however so do America’s prime cyber insurance coverage firms – and their efforts haven’t gone unnoticed.

In a panorama of relentless digital threats, Insurance coverage Enterprise America acknowledges the nation’s main cyber insurance coverage suppliers. 1000’s of brokers from throughout the nation supplied candid assessments of insurers’ efficiency in areas together with protection, adaptability, and claims dealing with. Solely the perfect of the perfect had been then awarded 5-Star standing.

“What resonates with brokers is that we’re greater than an insurance coverage service to their purchasers; we’re a full-service associate”

Jacob IngerslevTokio Marine HCC

Trade knowledgeable Michael Lieberman, co-founder and CTO of software program agency Kusari, shares his ideas on what a number one coverage seems to be like in 2025.

“It’s one thing that’s future proof at some degree, that’s evolving with the occasions as various kinds of cyberattacks turn into extra subtle. What’s additionally essential is being crystal clear about what is roofed and what’s not,” he says.

Fellow cyber insider Kelly O’Brien, senior cybersecurity practitioner at Compass IT Compliance, additionally defines what’s market main.

“It ought to be broad, adaptive protection together with particular concerns for AI utilization each internally and throughout third-party distributors,” she says. “It additionally goes past primary protection by together with proactive companies like risk intelligence, safety posture assessments, third-party danger instruments, and workforce consciousness coaching.”

Different key differentiators embrace:

Ransomware has turn into an excellent greater risk for cyber insurers in 2025 as they react to an uptick in assaults. A part of the rise is all the way down to the rise of ransomware-as-a-service (RaaS) and AI-powered variants.

The most typical is by a VPN compromise as risk actors scan Safe Sockets Layers (SSL), generally an internet web page log-in. From there, they use brute power and check out 1000’s of password combos a minute till they achieve entry.

“Upwards of 40 p.c to 50 p.c of ransomware assaults proper now happen that manner and it’s fairly a easy method. You don’t really want loads of sophistication,” says Jacob Ingerslev, head of cyber and tech underwriting at 5-Star 2025 insurer Tokio Marine HCC.

The opposite manner ransomware is utilized by risk actors is to focus on an enormous vendor, realizing they’ll have a big influence if they’ll exfiltrate knowledge.

“If the seller doesn’t pay up, then they’ll begin extorting the person clients,” provides Ingerslev.

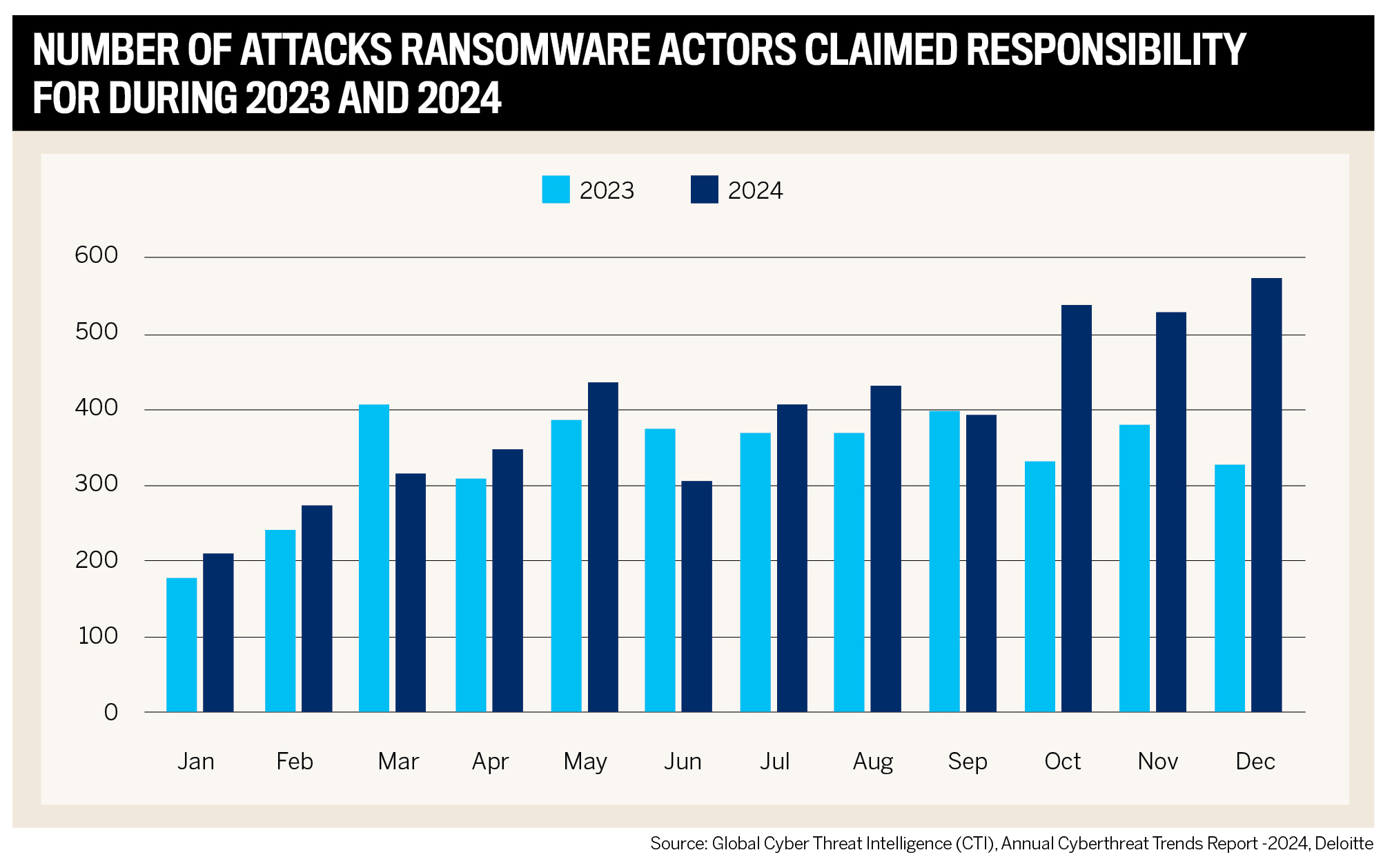

Deloitte’s annual Cyberthreat Tendencies Report noticed a 17 p.c improve in ransomware assault claims in 2024, peaking within the fourth quarter with 57 p.c extra claims in comparison with the fourth quarter of 2023.

This bounce is partly defined by the emergence of recent ransomware teams comparable to:

-

ALPHV

-

El Dorado/BlackLock

-

Lynx

-

Fog

-

APT73/BASHE

Some are judged to be nation state-sponsored cyber espionage, whereas others are financially motivated, which is one other space the place the perfect insurers have a job to play.

For instance, studies counsel that CDK International paid a $25-million ransom after a cyberattack in 2024 and edtech supplier PowerSchool confirmed it additionally paid out.

Tokio Marine’s knowledge exhibits a drop in ransomware assaults in 2022, however that has rebounded after which some.

“We noticed an enormous improve yr over yr in Q1 of 2025. We take a look at these so-called leak websites, or the ‘wall of disgrace,’ which is, when you pay the ransom, you don’t find yourself on the ‘wall of disgrace.’ In case you take a look at that in Q1 in 2025, there was an 86 p.c improve yr over yr,” Ingerslev says.

“We may also help with the negotiation if a ransom cost should happen. Usually, when all backups have been destroyed, that’s when you get thinking about [whether] it’s higher to pay the ransom, versus spending an exorbitant sum of money to rebuild the information from scratch.”

Specific industries that fellow IBA’s 5-Star Cyber winner Arch Insurance coverage has detected exercise in are healthcare and manufacturing.

“In healthcare, there’s know-how dependency on operations, in addition to loads of delicate knowledge and knowledge,” says Jamie Schibuk, government vice chairman, skilled legal responsibility and cyber. “We proceed to see assaults on the operational know-how that manufacturing firms depend upon, which regularly tends to be extra legacy-type know-how, which might create points if these networks are compromised.”

How America’s prime cyber insurance coverage firms navigate AI

Lieberman sheds gentle on how some risk actors benefit from AI hallucinations or how they seed the web with unhealthy knowledge to persuade new AI fashions to offer deceptive solutions.

He says, “You may ask ChatGPT one thing, and it provides you a solution which appears cheap to say, ‘Set up this software program’. It seems that software program was written by malicious actors, however you obtain it pondering, ‘I ought to get this software program instrument.’”

Nonetheless, the primary hazard from AI is refining and enhancing current threats, as insurers are primarily seeing it deployed in social engineering assaults, because the tech permits risk actors to good emails. Usually, criminals use AI to imitate the tone and elegance of emails between two events utilizing a big language mannequin (LLM), which extremely will increase the prospect of their e-mail being taken at face worth.

“It’s very simple to spin up a natural-sounding e-mail, notably if they’ve already breached the client’s inbox,” says Michael Drummond, chief underwriting officer cyber/tech at At-Bay. “Every new LLM mannequin that comes out, you see an uptick in monetary fraud as a result of it’s making it simpler to tug these issues off, because it’s lots tougher to distinguish between what’s a reliable e-mail and a fraudulent one.”

At-Bay, one other of IBA’s 5-Star insurers of 2025, combats this by combing by means of all of the claims which have resulted from some of these emails and utilizing their system to pinpoint indicators that counsel fraudulent exercise.

“We all know that 80 p.c of our monetary fraud claims come up from e-mail assaults, so earlier this yr, we launched a brand new e-mail safety resolution that’s accessible to each insured in our portfolio,” says Drummond.

“We’ve constructed all of our know-how in-house from the bottom up. So, not solely are we a full-stack insurance coverage firm however have a separate safety division that gives the entire safety companies to our insureds”

Michael DrummondAt-Bay

As a consequence of At-Bay’s scale of getting 40,000 enterprise purchasers, from startups to these with $5 billion in income, the instrument is powered by real-life claims knowledge that mirrors the threats firms are dealing with. The agency believes so deeply in its resolution that it’s keen to double and even quadruple the standard quantity of protection if purchasers undertake it.

“We’ve got entry to info that conventional safety suppliers and corporations don’t, as we are able to really see what actually drives some of these claims and what causes them,” provides Drummond. “We’ve got designed our safety resolution particularly to establish these traits.”

Arch Insurance coverage is even detecting the usage of deepfakes to facilitate financial institution transfers.

“The know-how is superior sufficient to idiot individuals into pondering that they’re speaking to the CFO of their firm, once they’re actually not,” says Schibuk.

His different concern with AI is that risk actors can leverage it to extend the size of their assaults. Remaining vigilant throughout this panorama is a every day concern for Arch. The agency has a 30-person underwriting group, however as well as additionally has a group of 4 cybersecurity danger engineers.

“All of them have a background working inside safety operation facilities of firms, so that they’re approaching it extra from the consumer facet. That’s actually useful in each the danger analysis in addition to serving to us to vet loads of third-party instruments and danger administration companies, as a result of they’ve precise implementation expertise in utilizing loads of these instruments,” says Schibuk.

And he provides that high-quality professionals are nonetheless the distinction makers.

“There’s loads of know-how and course of that we are able to leverage and implement, however on the finish of the day, a lot of it comes all the way down to our method to the enterprise and the folks that work on it day by day.”

Standout options of America’s prime cyber insurance coverage firms

Tokio Marine’s risk consciousness and remaining in line with all the newest developments depends on its Cyber Risk Intelligence group, which has the instruments to observe purchasers’ networks on an ongoing foundation.

The group has delivered for purchasers who’ve fallen sufferer to wire fraud switch, as over the past yr, it has recovered over $30 million by working with legislation enforcement and appearing quick. It is usually plugged into boards the place instrument kits are on the market that grant entry to methods.

This studying mindset is a aggressive benefit to the agency, because it frequently explores and discovers what risk actors are planning after which informs their insureds. One such manner is by way of honeypots – pretend machines on the web that seem like an precise firm with an precise server however are simply there to choose up exercise and study what risk actors are doing.

Ingerslev says, “That’s one strategy to study, and the opposite manner is to collaborate with individuals who function at nighttime internet boards. One firm we work with intercepts assaults by buying entry to clients from risk actors.”

There’s additionally nice profit from Tokio Marine’s in-house Incident Response Administration group that gathers forensic studies from all of the claims.

“We will decide what are the commonest causes of loss, and what are the commonest methods risk actors get right into a community, and in addition handle these. That suggestions loop is so essential,” says Ingerslev.

Highlighting simply how highly effective that is, Tokio Marine typically discovers software program vulnerabilities earlier than even the distributors of the know-how do.

Ingerslev provides, “In some circumstances, we’re quicker and it’s as a result of now we have the claims. That’s why we see it rapidly and now we have a really robust incentive to assist the purchasers, as a result of it helps us, too.”

Enabling brokers to ship

Arch prioritizes consciousness and ensures it places brokers in the very best positions with its purchasers.

Schibuk appreciates that brokers’ function has turn into tougher in cyber as a result of danger elements and advancing know-how.

“With all of the value-added companies, they’re serving to to facilitate that dialog, so that they’re a very key a part of the method and allow us to roll out loads of the danger administration companies.”

The trade has turn into extra technical over the previous 5 years and Arch’s Built-in Danger engineering group has turn into extra subtle across the questions it asks and the instruments it makes use of to judge.

“We’re positively a really entrepreneurial sort of firm. We take delight in being inventive on how we method danger,” says Schibuk. “We’ve got a extra versatile method than loads of others within the market, together with the power to customise protection for particular person insureds.”

“There’s no commonplace cyber coverage. Each single one is completely different, and we work actually intently with our brokers to customise protection, relative to what an insured’s particular person danger profile is”

Jamie SchibukArch Insurance coverage

This mentality extends to At-Bay, the place the group is targeted on enabling brokers to grasp the safety posture of purchasers. The group ensures that brokers perceive its merchandise and what places firms in danger from cyber threats.

The At-Bay group views itself as a useful resource for brokers to lean on.

“We’re completely satisfied to interact at no matter degree they need, from very deep technical conversations to only ensuring who’re the precise individuals to name or hand the client off to in the event that they’re not as comfy, entering into the weeds on a number of the cybersecurity stuff,” says Drummond.

Giving brokers license to customise merchandise is one other service that At-Bay brings to the desk. Its software program engineers and builders constructed the corporate’s complete underwriting platform, claims system, and safety platform. This affords them the power to have a good suggestions loop throughout all enterprise operations.

Its InsurSec resolution, At-Bay Stance™, is a unified safety platform that helps insureds proactively establish and mitigate cyber dangers related to 86 p.c of buyer claims. Entry is included with each Cyber and Tech E&O coverage and gives an estimated worth of as much as $72,000 per yr in safety options.

Earlier this yr, At-Bay additionally launched two new InsurSec options designed to fight the commonest sort of cyber declare: monetary fraud. These instruments assist forestall fraud earlier than it occurs and might unlock enhanced protection phrases for eligible insureds, together with monetary fraud sublimits of as much as $1 million.

On the core is the agency’s ethos of responsiveness and demanding pondering.

Drummond says, “Whether or not that’s a extra complicated or much less complicated account, our people are there to have these conversations they usually aren’t afraid to assume exterior of the field and tailor one thing.”

Flexibility, responding rapidly and operating instructional webinars are methods Tokio Marine helps its brokers. The agency can be content material to be clear about what it does and what it will possibly supply.

“Even when a competitor is aware of our strategies and method to consumer monitoring, alerting and the incident response, it will nonetheless take them a very long time to construct one thing related. So, we’re comfy,” says Ingerslev.

Tokio Marine’s main goal market is the small to mid-sized segments that may use the insurer’s preventative companies, in comparison with a Fortune 1000 firm that’s prone to have in-house cyber groups.

This yr’s recognition is the fifth successive annual cyber award for Tokio Marine, which helps its view that its infrastructure and methods in place are formidable.

“It’s a stamp of high quality and in addition an indication of consistency,” provides Ingerslev. “We’re an enormous world insurer with very stable monetary stability behind us, and that permits us to proceed to remain related and have an inexpensive market share, but additionally not fall into some traps in elements of the market cycle.”

Each trade specialists – Lieberman and O’Brien – who spoke to IBA for this report agree that cyber insurance coverage has not but reached the maturity the place it exists alongside extra established areas comparable to flood or fireplace.

O’Brien says, “They’re backed by many years of actuarial knowledge, however cyber insurance coverage remains to be evolving as a result of fast tempo of technological change and the volatility of cyber threats. Many incidents go unreported, and the danger panorama continues to shift, making it tougher to standardize and stabilize the market to the identical diploma.”

Lieberman additionally factors to the quickly evolving nature of the market, which makes it troublesome to outline protection and results in confusion.

“If a brand new sort of assault is found, is that coated robotically? The problem for lots of insurance coverage firms is that the state of issues is altering so quick,” he says.

And he additionally cites that the cuts to authorities businesses centered on compliance and rules within the cyber safety house is resulting in considerations. For instance, Nationwide Institute of Requirements and Applied sciences (NIST) misplaced a whole bunch of cybersecurity workers on account of downsizing. A part of its function is to run the Nationwide Vulnerability Database, which some concern could disappear sooner or later.

Liberman provides, “If it does go away, what will be there’s unclear. That’s an enormous drawback for insurance coverage firms, as a result of they’re viewing this as if in case you have vulnerabilities that exist within the database, and it is advisable to repair them. But when that goes away, what are they going to make use of as a gauge to say you’ve got this vulnerability?”

- AIG

- AXA XL

- Beazley

- CFC

- Chubb

- Cowbell

{kind=link}