Within the period of cutting-edge laptop modeling, satellite tv for pc information and AI, there has by no means been extra considerable data on the hazard that wildfire poses to houses within the Los Angeles space. However that didn’t essentially assist hundreds of householders accurately assess their private danger.

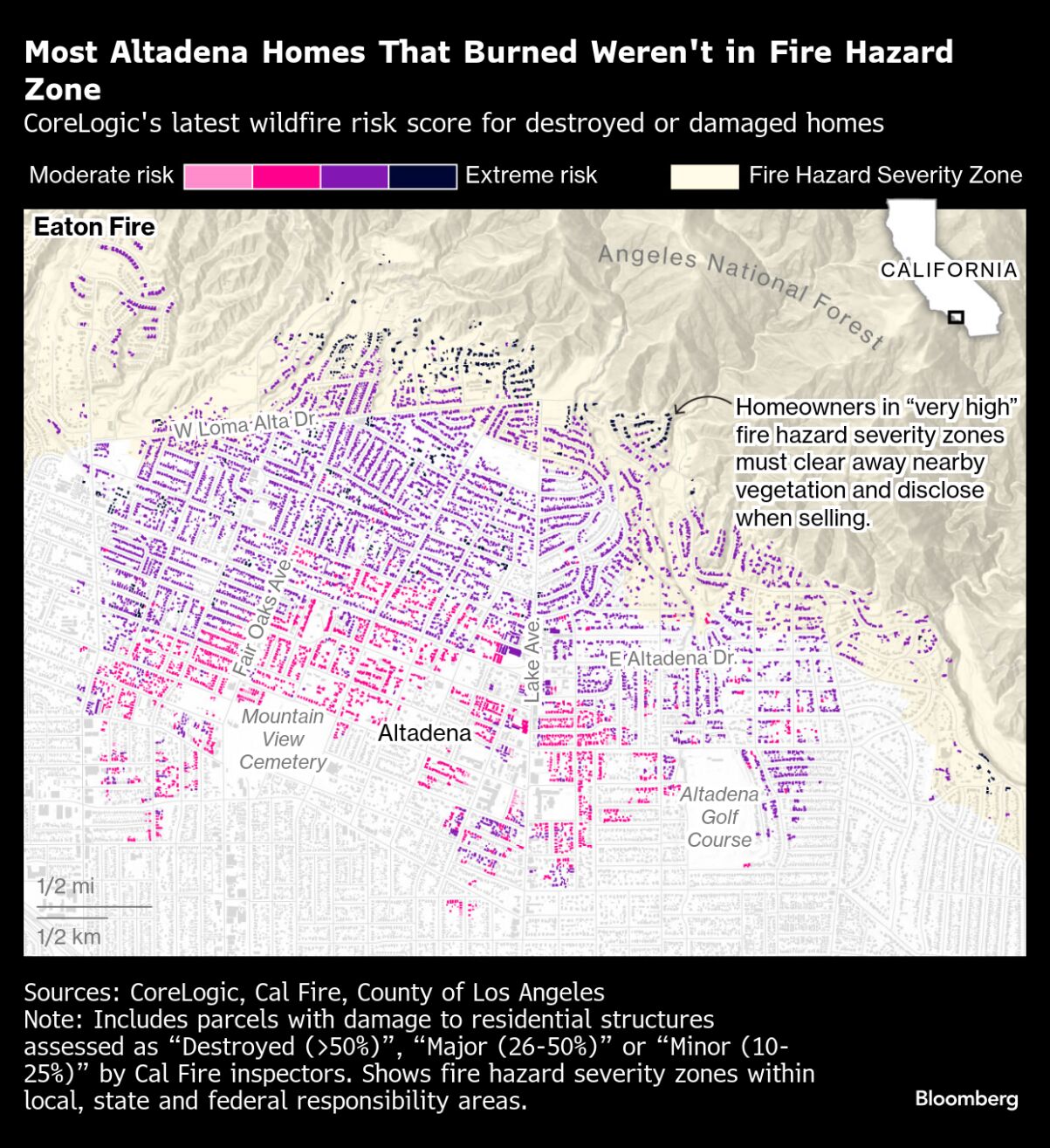

Many houses that burned within the Eaton Fireplace lay outdoors the boundaries of state- or local-designated “very excessive” fireplace hazard severity zones, Bloomberg Inexperienced discovered after analyzing inspection experiences by the California Division of Forestry and Fireplace Safety, or Cal Fireplace, for greater than 20,000 residential properties in areas affected by the current wildfires.

Associated: Munich Re Faces $1.3 Billion in Claims From Los Angeles Wildfires

The fires final month destroyed greater than 11,000 houses in whole, and greater than 40% of these had stood outdoors of the official fire-hazard zones. In Altadena, some 4,500 homes burned in places past the zone boundaries. Meaning householders confronted no fire-related disclosure necessities when buying a house, as could be the case for transactions contained in the zones. Property house owners contained in the zone additionally face mandates for brush clearing and different steps to mitigate danger that didn’t apply to close by houses outdoors the boundary.

Insurers had entry to extra finely tuned danger indicators, and knew learn how to interpret them. The neighborhoods that burned in LA “appeared disproportionately excessive danger in comparison with the remainder of the nation, and insurers knew it,” says Anand Srinivasan, head of analysis and growth at CoreLogic Inc., a property data firm.

This hole factors to a wider downside. As climate-driven perils akin to wildfire and flooding turn into extra frequent and extra extreme, many extra People will attempt to assess their residence’s vulnerability. They’ll face combined alerts and a disparity between what information is freely out there and the fuller information that personal corporations pays to entry.

The federal government fireplace hazard maps of LA are simply discovered on-line. Different, extra exact data on fireplace danger in LA neighborhoods exists within the non-public sector. CoreLogic, which consults for presidency and insurers, amongst different purchasers, had rated the overwhelming majority of houses in Altadena as having a “excessive” or “very excessive” danger of wildfire injury — even when they lay outdoors a hazard zone.

However this information isn’t out there to most of the people. It’s bought business-to-business; CoreLogic made it out there to Bloomberg for this story.

Associated: Insurers Have Now Paid Out Practically $7B for LA Wildfires, Report Exhibits

There have been different locations householders nervous about wildfire danger may discover extra data, in the event that they had been motivated. First Avenue Expertise Inc. estimates local weather dangers on the property degree and makes its danger scores out there to the general public totally free. Its danger scores seem in listings on the favored actual property websites Zillow and Redfin.

About 95% of destroyed houses in Altadena had a hearth danger degree of not less than 7 on a 10-point scale as assigned by First Avenue.

However even individuals who see greater scores won’t absolutely grasp them or can discover methods to downplay them.

“While you give individuals numbers like this, they have an inclination to numb,” says Anthony Leiserowitz, the founding director of the Yale Program on Local weather Change Communication. “Particularly in the event that they’re not based mostly immediately on somebody’s personal expertise.”

Associated: California Approves FAIR Plan Request to Assess Insurers $1B for Wildfire Claims

Individuals are inclined to low cost hazard that’s not rapid. Whereas a majority of People say that world warming is already taking place, solely 47% consider that it’s inflicting hurt within the US “proper now,” in accordance with current analysis. In different phrases, individuals are inclined to see local weather change as an issue of the longer term although it’s already wreaking injury.

Local weather change made the LA fires considerably extra more likely to occur, scientists have concluded, and intensified final 12 months’s ferocious Hurricane Helene. “We research local weather change and we all know that it’s altering the chances in all these elementary methods,” Leiserowitz says, “however most individuals don’t perceive that.”

Local weather danger can also be tough to convey as a result of it’s decrease within the very close to time period than over a lifetime, or the standard size of a mortgage. For instance, what’s typically referred to as the 100-year floodplain will not be an space that floods roughly as soon as a century, as is usually assumed. It’s an space the place the danger of flooding is 1% a 12 months, and over 30 years, that probability quantities to 1 in 4.

Complicating the image additional, present ranges of local weather danger aren’t fixed. They are going to rise as extra greenhouse gases are pumped into the environment. Threat modelers account for this of their projections.

Arguably, the clearest sign for LA householders was being positioned in a hearth hazard severity zone. However shiny boundary traces will be lulling to these simply on the opposite aspect of them.

Doug Mark, a resident of West Hollywood, lives lower than a block from the place Sundown Boulevard marks the beginning of a zone. He says it’s not of nice concern to him and his neighbors, and that he hasn’t had bother getting or maintaining insurance coverage.

“Even if you happen to’re 5 minutes from the hills, I don’t suppose there’s any situation. As quickly as you cross Sundown Boulevard, that’s when persons are occupied with it,” he says.

Altadena sits on the edge of 1 “very excessive” severity zone. Eighty p.c of the native houses that burned sat outdoors the zone.

Cal Fireplace takes pains to clarify that danger ranges and hazard zones aren’t the identical factor. Hazard zones are mapped based mostly on bodily circumstances that create a chance of fireplace, and the anticipated habits of potential fires, over a 30-to-50-year interval. That course of doesn’t keep in mind attainable mitigation measures akin to residence hardening or gas discount, which may change the danger.

Matthew Eby, the founder and president of First Avenue, says the corporate thought quite a bit about learn how to talk danger, selecting a 1-to-10 scale for simplicity, paired with descriptors akin to “reasonable” or “extreme.” Nonetheless, its estimates are simply that. Each danger modeler approaches the duty in a different way and sometimes with completely different inputs. A previous Bloomberg evaluation of estimates of flood danger in Los Angeles — together with by First Avenue and CoreLogic — discovered vast discrepancies between them. And wildfire danger is extra complicated to mannequin than flood danger.

Eby says that since insurers and monetary establishments have entry to property-level danger estimates, it’s solely honest for householders to have it, too.

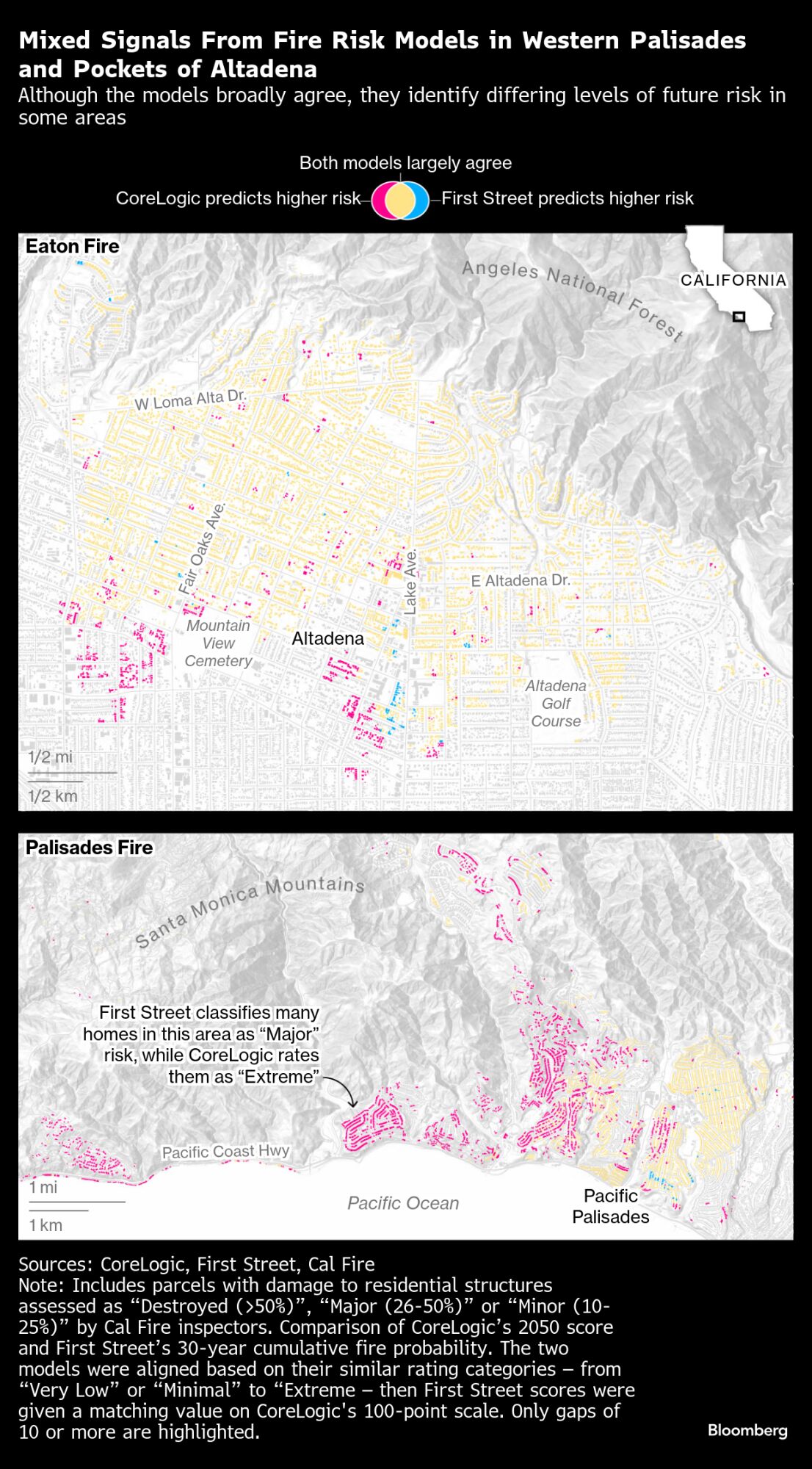

Blended Alerts From Fireplace Threat Fashions in Western Palisades and Pockets of Altadena | Though the fashions broadly agree, they establish differing ranges of future danger in some areas

Whereas First Avenue assesses the relative danger of fireplace occurring on a given property, CoreLogic calculates its scores based mostly on the projected prices of repairing or rebuilding because of wildfires and smoke over time. CoreLogic can estimate present danger or have a look at danger going into the longer term. (In contrast, First Avenue’s danger scores are designed to seize cumulative danger over 30 years.)

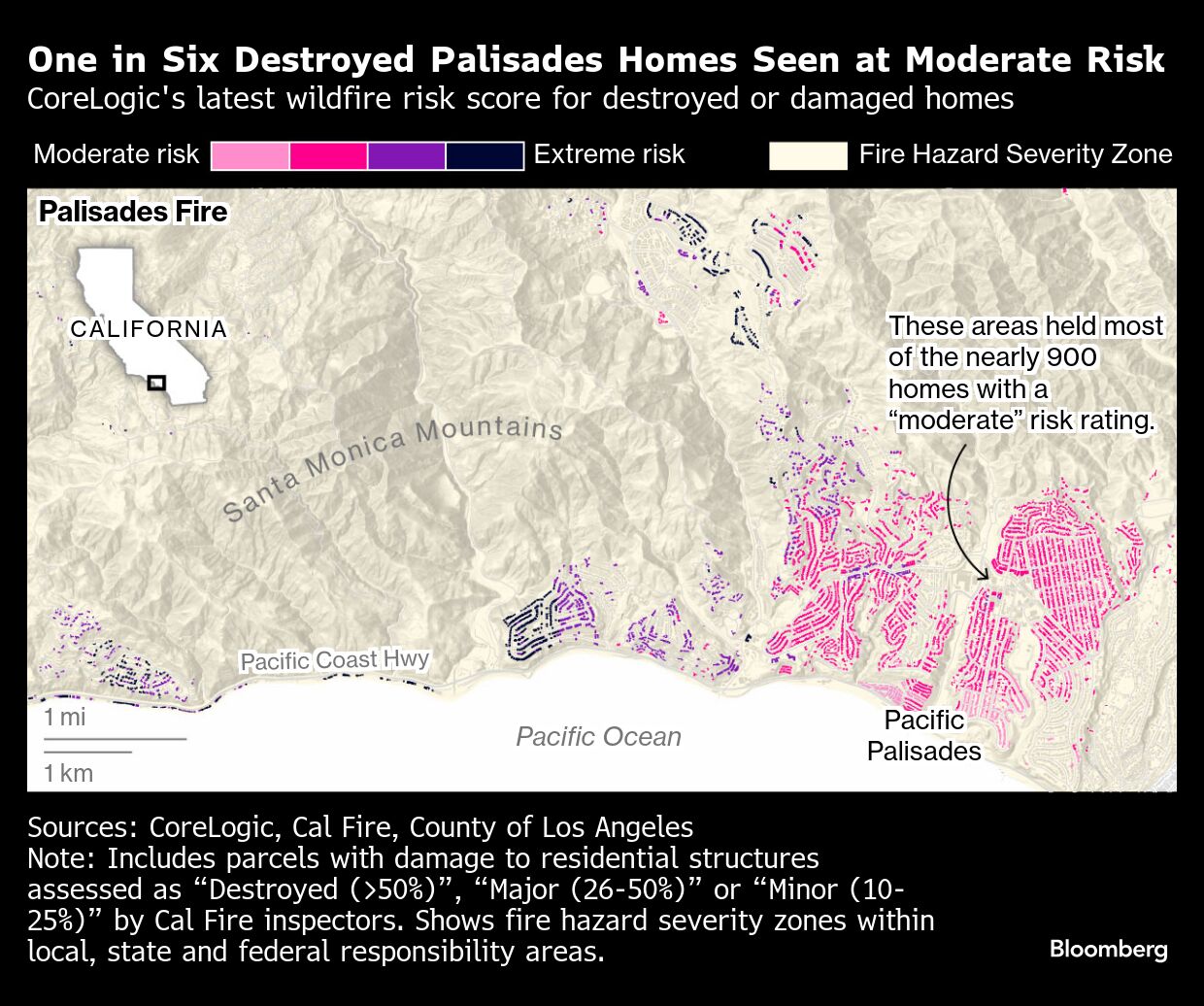

Additional west, all the space leveled by the Palisades Fireplace was coated by state or native fireplace hazard severity zones. But about 850 of the houses destroyed, or 15% of the overall, had a present wildfire danger rating from CoreLogic within the “reasonable” vary, between 36 and 55 out of 100. Many of those houses had been clustered within the jap areas of the fireplace’s path, within the Pacific Palisades neighborhood correct. In contrast, additional west in Malibu, one in three houses had an “excessive” rating of 86 or greater.

The catch is that whereas abnormal residents are inclined to low cost danger scores, insurance coverage corporations completely don’t. They usually don’t measure it the identical means, both. Insurers are a liquid pool of capital with no emotional attachment to houses; it’s their enterprise to be ruthless of their analytical assessments.

Even a “reasonable” CoreLogic rating would ship a robust sign to an insurance coverage firm. Absolutely 70% of houses throughout the US scored by CoreLogic have fireplace danger under “reasonable.” Insurers additionally look not solely at averages however on the tail of the curve, which is possible most loss.

Though a share of the houses had decrease scores, says CoreLogic’s Srinivasan, “the majority had been greater, and whenever you couple that with 80-mile-an-hour sustained winds and the proximity of the properties, you’re going to have a extreme impression on even lower-risk properties.”

Insurers had already been pulling out of Pacific Palisades. State Farm, California’s largest residential insurer, moved to cancel practically 70% of its insurance policies in a single Zip code there final 12 months. (The corporate paused non-renewals after the fires, in response to a moratorium issued by the state.)

In concept, high-priced insurance coverage or a scarcity of insurance coverage choices ought to be one other clear message to householders that they’re in hurt’s means. However, says Yale’s Leiserowitz, it’s attainable to place that down principally to insurance coverage firm greed.

Marcy Weinstein, an actual property agent in fire-prone Newport Seaside, south of LA in Orange County, says her purchasers typically interpret it that means.

After the fires in LA, “I’m not seeing an enormous degree of hysteria occur,” she mentioned. “What we’re seeing is backlash towards the insurance coverage being so tough to get. You’re attempting to get your dream residence, and it’s tough for insurance coverage to match up.”

Copyright 2025 Bloomberg.

Subjects

Louisiana

{kind=link}